The End of an Era: Social Security’s Shift to Direct Deposit

For decades, the familiar crispness of a Social Security check arriving in the mail has been a reassuring ritual for millions of Americans. This dependable monthly arrival, often a lifeline for seniors and disabled individuals, represented more than just a financial transaction; it was a symbol of security and stability in the face of life’s uncertainties. However, a significant change is on the horizon, one that could impact the lives of hundreds of thousands of individuals.

The government is phasing out paper checks as a method of delivering Social Security benefits. While this may seem like a minor adjustment in our increasingly digital world, the implications are far-reaching and potentially disruptive for a considerable segment of the population. The transition to direct deposit, while efficient and cost-effective for the government, presents significant challenges for those who lack bank accounts, are unfamiliar with technology, or lack the support to navigate the necessary steps.

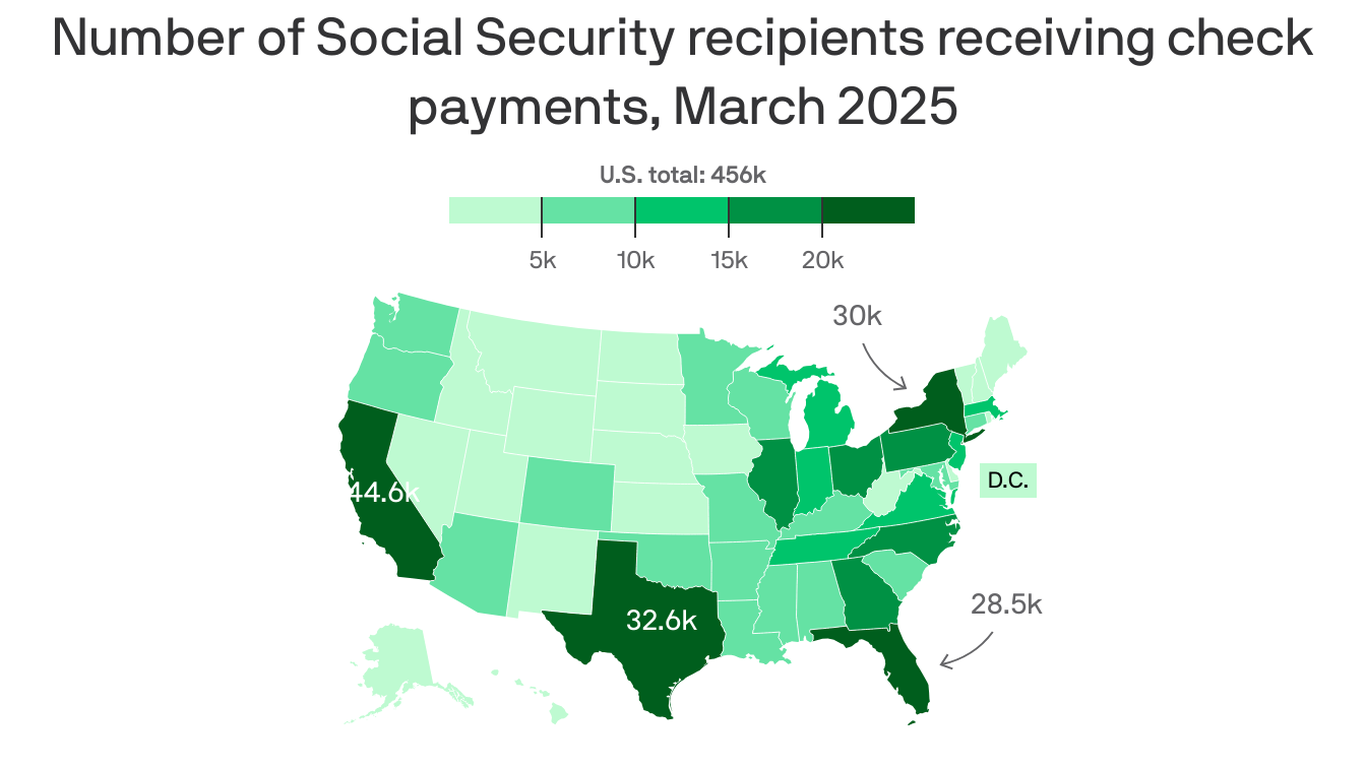

Estimates suggest that nearly half a million Americans currently receive their Social Security payments via paper check. This isn’t a negligible number; it represents a substantial portion of the population who rely on this traditional method for receiving their benefits. For these individuals, the shift to direct deposit presents a range of difficulties. Many lack access to bank accounts, facing barriers such as minimum balance requirements, fees, and inconvenient branch locations. For those in rural areas or underserved communities, these obstacles are particularly pronounced.

Furthermore, the transition demands a level of technological literacy that some recipients may not possess. Navigating online banking platforms, setting up direct deposit, and understanding the intricacies of online financial management can be daunting for older adults or individuals with limited computer skills. This digital divide exacerbates the challenges, leaving vulnerable populations at risk of experiencing delays, errors, or even complete disruption to their income stream.

The potential consequences of this shift extend beyond mere inconvenience. For many seniors and disabled individuals, Social Security benefits constitute their primary source of income. Any disruption to the timely receipt of these funds can have devastating consequences, affecting their ability to afford essential necessities such as housing, food, and medication. The stress and anxiety associated with navigating this change, especially during a time of already strained resources, should not be underestimated.

The government has a responsibility to ensure a smooth and equitable transition for all affected individuals. Simply announcing the change and expecting everyone to adapt seamlessly is insufficient. A comprehensive support system must be implemented, providing assistance to those who need it most. This may involve outreach programs to educate beneficiaries about the change and assist them in setting up direct deposit accounts. Collaboration with community organizations, banks, and financial literacy programs is crucial to bridge the digital divide and prevent individuals from falling through the cracks.

Ultimately, the shift away from paper checks necessitates a focus on inclusivity and accessibility. While the benefits of direct deposit are undeniable, ensuring that all recipients can seamlessly transition to this new system is paramount. A failure to adequately support those who rely on paper checks risks leaving vulnerable individuals behind, undermining the very security and stability that Social Security is intended to provide. A compassionate and well-planned transition is not just desirable, it’s essential.

Leave a Reply